As a boutique small-cap manager focused on responsible investing, we’ve seen firsthand the challenges small-cap companies face in publishing sustainability data. But, since our inception in 2016, the tide has been shifting.

The rapid growth of small-cap companies reporting on sustainability is evident. Yet, a critical gap remains: there’s still a lack of transparency on which companies are leading the way and which industries are lagging. In response to this gap, we took matters into our own hands and initiated a comprehensive data collection project covering all Russell 2000 companies, culminating in the findings presented here as of June 1, 2024.

Key Takeaways

-

While sustainability reporting has become the norm among large-cap companies, a promising 50% of Russell 2000 firms now publish ESG data.

-

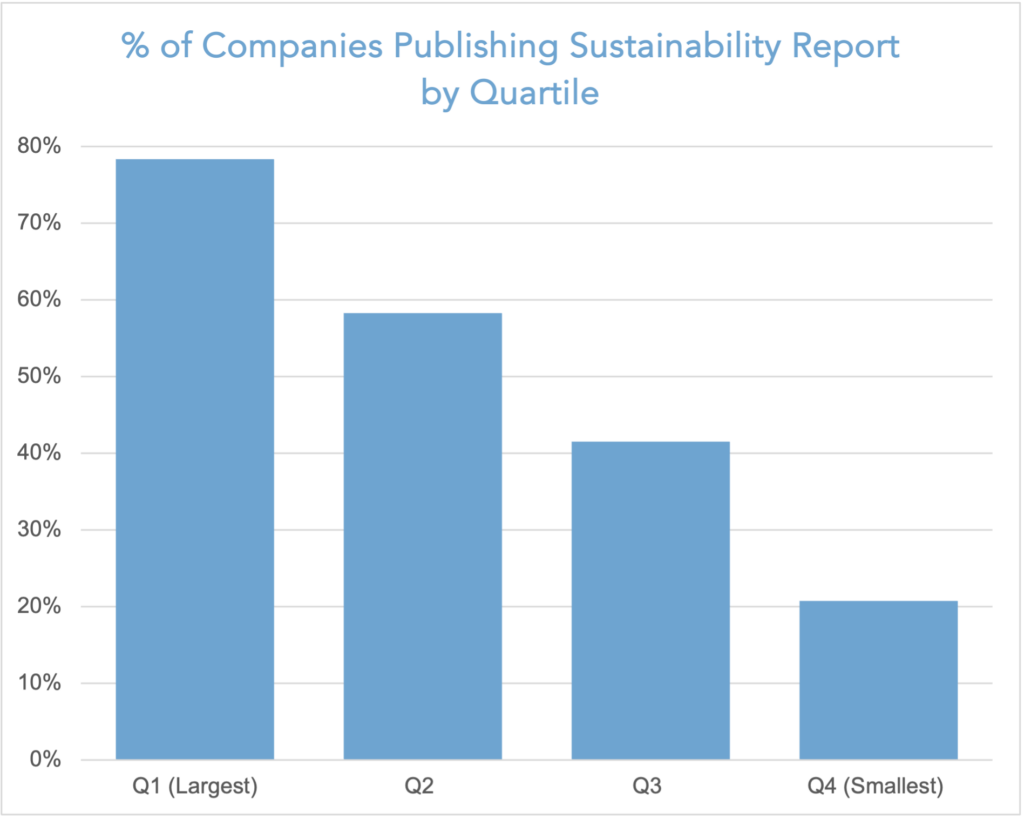

Larger small-cap firms are leading the charge, with over 78% of companies in the top quartile reporting, compared to just 21% in the bottom quartile.

-

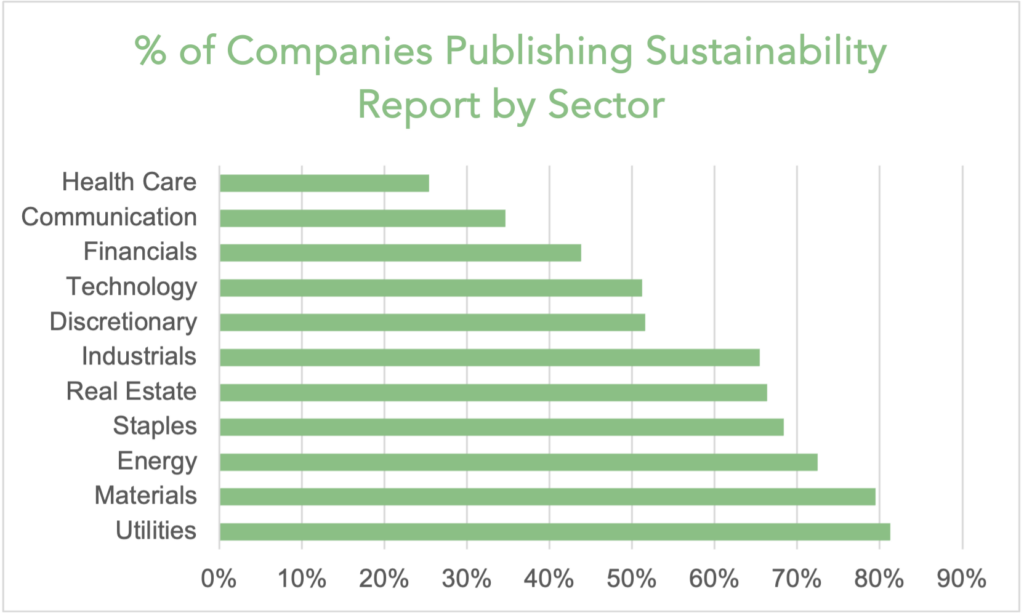

Sector differences are stark, with resource-intensive industries like energy and materials far outpacing service-oriented sectors like healthcare and tech.

-

The Sustainability Accounting Standards Board (SASB) has emerged as the preferred reporting framework, utilized by 35% of disclosing firms.

A Glass Half-Full for Small-Cap Sustainability

The sustainability reporting revolution continues to sweep through Corporate America, with nearly all S&P 500 companies now publishing environmental, social, and governance (ESG) data. However, the small-cap universe tells a different story.

Source: Riverwater research. Source file available by request.

Our analysis of Russell 2000 constituents reveals that only around 50% of these smaller firms have embraced sustainability disclosure. This is a sharp contrast to their large-cap peers. This gap is concerning, as investors increasingly demand transparent ESG performance data to inform their capital allocation decisions.

The reasons for this disparity are not hard to discern. Smaller companies often lack the resources and expertise to navigate the complexities of sustainability reporting. Building the necessary data collection and reporting infrastructure requires significant time and financial investment – a tall order for cash-strapped, growth-stage firms.

Size Matters, But Sector Divides Run Deep

Digging deeper into the data, a clear correlation emerges between company size and reporting rates. Over 78% of firms in the Russell 2000’s largest market cap quartile now publish sustainability reports, compared to just 21% in the smallest quartile. This suggests that as small-caps mature and gain scale, they are more likely to prioritize ESG transparency.

However, sector differences create an even more nuanced picture. Resource-intensive industries like energy, materials, and utilities lead the way, with over 70% of constituents reporting. In contrast, service-oriented sectors like healthcare, communications and financials lag significantly, with less than 40% of firms disclosing.

The reasons for these divergences are multifaceted. Capital-heavy industries face more pressure to prove their environmental responsibility. In contrast, service firms often see sustainability reporting as less relevant to their business. Regulatory influences also play a role, with certain sectors facing more stringent ESG disclosure mandates.

Source: Riverwater research. Source file available by request.

SASB Leads

As small-cap firms have stepped up their sustainability efforts, they have also grappled with the question of reporting frameworks. Our data reveals that the Sustainability Accounting Standards Board (SASB) has become the clear favorite, with 35% of disclosing Russell 2000 companies utilizing this investor focused and industry-specific standard. In contrast, the broader Global Reporting Initiative (GRI) framework is used by just 18% of reporting firms. This preference for SASB underscores the desire among small-caps for ESG metrics that are material and decision-useful for their particular businesses and the investment community.

The Road Ahead

While the sustainability reporting gap between large and small-cap firms remains wide, pockets of progress are emerging. As smaller companies gain scale and face mounting stakeholder pressure, we expect sustainability disclosure rates to continue climbing. However, sector-specific dynamics and resource constraints will likely sustain uneven adoption across the Russell 2000.

To close this gap, policymakers, industry groups, and sustainability advocates must redouble efforts to provide small-caps with the tools, guidance, and incentives necessary to embrace ESG transparency. Only then can investors gain a comprehensive view of sustainability performance across the entire public equity landscape.