Winning the AI Race: Why Infrastructure Beats Talent

(July 14, 2026).

To Win Global, Build Local

After watching a handful of the 2026 FIFA World Cup games, it’s apparent that no team wins a World Cup on talent alone. Even a casual observer (like me, who hasn’t watched this much soccer since the TV series Ted Lasso) can see that the teams still standing aren’t always the most talented. They are the ones with the depth, the systems, and the organizational infrastructure built long before kick-off. The same is true of how FIFA selects its host countries. The nations awarded hosting rights aren’t necessarily those with the most passionate fans or the most soccer-savvy populations. They’re the ones with the stadiums, the transit systems, and the civic infrastructure to actually carry the weight of an event at this scale.

Often, World Cup Championships, and competitive advantages in business, go to whoever built the foundation long before anyone was watching.

We think that same logic can be applied to the biggest competition in markets today: the race to build, power, and deploy artificial intelligence at scale. The companies and countries that ultimately “win” that race won’t just be the ones with the best models. They’ll be the ones with the grid capacity, the power generation, and the data center footprint to actually run the workloads. The global prize gets won locally, and this quarter, we made a portfolio change that reflects exactly that thesis (discussed later in this letter).

How Local Infrastructure Powers Global Events — and AI

The World Cup made its return to American soil this summer for the first time in over three decades, capturing the attention of billions and sparking an economic surge measured in the tens of billions across our metro areas. It is easy to overlook the hyper-local effort behind the spectacle. Across the eleven U.S. host cities, municipal bonds have been the quiet engine for the essential work. They have financed rail extensions, airport growth, and media hubs that will serve these communities long after the final whistle. In Seattle, the world’s first floating light-rail bridge opened this March. The nearly decade-long project was funded by federal grants, voter-approved regional taxes, and municipal bonds and completed before more than 750,000 visitors arrived. Dallas, the tournament’s busiest hub, transformed its convention center into a global media nerve center through $2.2 billion in bonds backed by local hotel revenue taxes.1 While federal aid played a part, it was only a fraction of the total cost. The heavy lifting fell to municipal issuers willing to finance the unglamorous plumbing required for a world-class event.

None of that infrastructure is a part of the actual game itself. But none of the game happens without it. The strongest host cities weren’t just the ones that could fill a stadium, they were the ones that had spent years building the fiscal foundation and capital infrastructure to absorb an event of this scale.

The Same Blueprint, Bigger Stakes

We see the race for artificial intelligence following this same blueprint, just on a far larger scale. Headlines focus on the latest chips and breakthrough models, but the underlying reality is a physical buildout: transmission lines, power generation, and data center footprints. By some estimates, energy demand for these centers is expected to quadruple by 2030, and utilities are already facing supply constraints while new grids are laid. An algorithm cannot conjure this capacity into existence. Meeting it will take the same capital-intensive, physical labor that built the broadcast hubs in Dallas and the rail lines in Seattle.

This expansion requires an “all of the above” strategy because the demand is too great for any single source. Renewables are the majority of new capacity being added, but nuclear, natural gas, and grid updates all have a major role to play.

So how did the quarter’s scoreboard actually read?

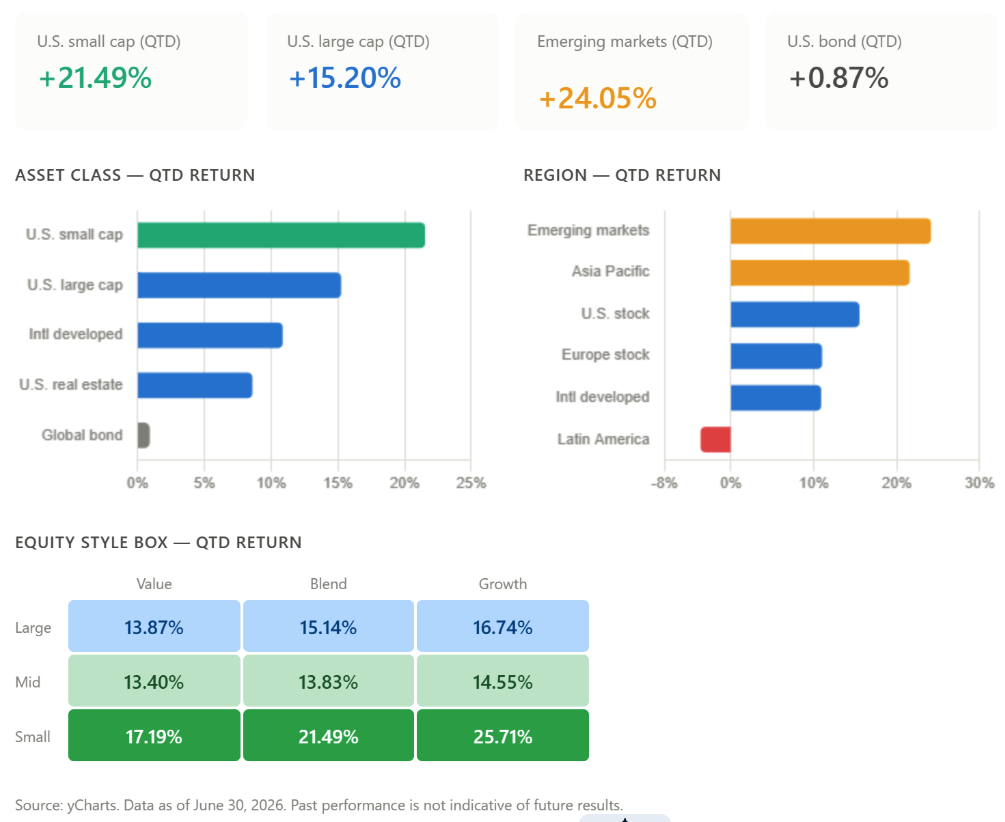

Q2 2026 Market Recap: Small Caps Surge, Breadth Deceives

The second quarter provided a nuanced look at market returns, which weren’t quite as broad-based as they seemed. Small caps posted a robust 21.49%, outpacing the 15.20% from large caps in a rally that saw value and growth both participate. This is the exact type of breadth that diversification is meant to provide after years of mega-cap dominance. However, the year-to-date data shows a significant shift: large cap value has returned 16.26%, while large cap growth has lagged at just 5.33%, mostly reflecting the first quarter’s rotation into value amid heightened geopolitical tensions in the Middle East.

The international landscape was even more complex. While emerging markets appeared to lead with a 24.05% return, a closer look reveals the same concentration we’ve seen stateside. Semiconductor heavyweights like TSMC, SK Hynix, and Samsung drove these benchmarks, meaning much of that return was simply the AI trade under a different name. Even markets that seemed diversified were often just another way of betting on the same small group of companies powering the digital buildout.

Fixed income remained remarkably quiet, with domestic bonds returning only 0.62% and global bonds sitting slightly negative for the year. In an environment where equities reached double-digit gains, traditional bonds provided ballast and small levels of income, but haven’t been drivers of return so far in 2026. This reinforces our strategy of seeking out alternative investment sources with lower volatility.

Our Q2 Move: Adding Global Infrastructure (VCRIX)

Instead of chasing those narrow market leadership, we integrated NYLI CBRE Global Infrastructure (VCRIX) into our models this quarter. Our goal is to own the “host city” layer of the AI expansion, rather than gambling on the individual athletes.

VCRIX targets the essential infrastructure that operates under regulated or long-term contracts: utilities, power grids, data center properties, and energy pipelines. This creates a risk profile fundamentally different from the tech giants. We believe the strategy can help reduce portfolio volatility relative to global markets while providing income. In our view, it also trades at a more reasonable valuation than the sector’s high-fliers. Rather than trying to pick the winner of the game, we like to think of it as investing in the concessions that fuel the fans.

What This Means for Your Portfolio

For our clients’ portfolios, this addition plays a supporting role: a steadier way to participate in the AI buildout alongside our existing equity exposure. Like any investment, infrastructure carries its own risks (interest-rate sensitivity, regulatory changes, and sector concentration among them) and the fund can lose value.

While we still maintain exposure, we aren’t trying to guess which specific chip or large language model (LLM) will come out on top. We believe with much higher conviction that regardless of the winner, they will all need the power and the data centers to function.

The Decade Ahead: Building Foundations for AI Growth

The team that eventually hoists the World Cup trophy won’t simply be the one with the most raw talent. It will be the team that had the depth and the infrastructure to perform when the pressure was highest. Every side left in the final four boasts a generational talent — Mbappé for France, Kane for England, Messi for Argentina — but none of them will win on a single star alone. It’s the players around them, and the youth programs, academies, and federations that developed that depth, that will decide who’s still standing on July 19th. We see the coming decade of investing in the same light. The winners in the AI era will be those who quietly established the foundations for growth long before the rest of the world was paying attention. That is where we are focusing a portion of your capital.

And for those looking for a distraction while we wait for the results of the AI arms race, Ted Lasso returns this August. I know I’ll be tuning in.

As always, thank you for your continued trust and partnership.

Connor Doak, CFA

Client Portfolio Manager

BLUE Impact Update — Q2 2026

To underscore our commitment to making the world a better place through responsible investing, we spotlight a positive impact achieved by one of our fund managers through their sustainable investments. This quarter’s example comes from Impax Asset Management, a manager built on its belief that investors who better understand sustainability risks and opportunities can generate superior long-term returns — a philosophy it puts to work through direct company engagement, proxy voting, and policy advocacy.

A recent case is Impax’s engagement with DSM-Firmenich, a Swiss specialty chemicals company supplying ingredients to the nutrition, health, and beauty industries. Engaging with the company since 2021, Impax focused its 2025 dialogue on encouraging a comprehensive assessment of DSM-Firmenich’s nature-related dependencies, impacts, risks, and opportunities across its value chain. The goal was to help the company better understand where biodiversity and water-related risks were most concentrated, and to integrate those findings into its broader nature strategy.

Following sustained engagement, DSM-Firmenich undertook a thorough assessment aligned with leading international frameworks, including the Taskforce on Nature-related Financial Disclosures (TNFD) and the Science Based Targets Network. The company determined that approximately 95% of its nature-related impacts stem from upstream agricultural raw materials, and it committed to strengthening its biodiversity and restoration efforts and continuing to monitor material sourcing risks.

Impax’s engagement process reflects how sustained dialogue and partnership can drive improvements in corporate risk management and resilience, while helping safeguard the ecosystems which society and economies depend on.

Citations

The information contained herein represents the opinion of Riverwater Partners and should not be construed as personalized or individualized investment advice. Analysis and opinions expressed in this letter are subject to change without notice. The securities and funds identified do not represent all securities purchased, sold, or recommended for client accounts, and the reader should not assume that investments in the securities identified were or will be profitable.

This letter contains forward-looking statements reflecting our current views and expectations. Actual results may differ materially, and we undertake no obligation to update these statements.

Market and index returns referenced herein are sourced from Ycharts as of June 30, 2026. “Small caps” refers to the Russell 2000 Index, “large caps” to the S&P 500 Index, “emerging markets” to the MSCI Emerging Markets Index, and “domestic bonds” to the Bloomberg U.S. Aggregate Bond Index. Indices are unmanaged, do not reflect fees, and cannot be invested in directly.

Investors should consider the investment objectives, risks, charges, and expenses of any fund carefully before investing. The prospectus contains this and other important information and should be read carefully. Investments in infrastructure-related funds are subject to risks including interest-rate sensitivity, regulatory change, and sector concentration. Yield fluctuates and is not guaranteed. Riverwater Partners receives no compensation from NYLI/CBRE in connection with this investment.

The Impax Asset Management engagement example is drawn from Impax’s published stewardship reporting, is provided for illustrative purposes, and does not represent the experience of Riverwater clients or guarantee any environmental or investment outcome.

Third-party information is obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. Riverwater Partners LLC is a registered investment adviser. Registration does not imply a certain level of skill or training. Past performance does not guarantee future results.