When Does Being “Safe” Become the Riskiest Move You Can Make?

Money can be emotional. I say that a lot, and I mean it every time. An example of where I have felt this clearly is a conversation I had a few years ago.

A very smart and thoughtful client, someone I genuinely respect, told me that before we started working together, he’d moved everything to cash in early 2022. The market was dropping, the headlines were relentless, he wanted to “hold on tight” to what they had, and under the circumstances stepping to the sidelines felt like the only reasonable thing to do to protect his family’s wealth.

“I was just waiting for things to settle down,” he said.

I understand the situation. When the market is falling, every instinct you have says stop the bleeding. Moving to cash or Treasuries feels decisive. Controlled. Like you’re doing something to address the problem.

I’ve sat across from enough people over the years in that position to know it’s not an irrational decision. It’s a very human one. But what I’ve learned, after 20 years of having these conversations, is that the decision that feels like the safest move often carries a cost that’s a lot harder to see. And this hidden cost is exactly what we hope to illuminate before it does irreversible damage to a client’s long-term goals.

What Waiting for “Clarity” Actually Looks Like

Here’s something I’ve noticed over and over again. A client steps out of the market when things feel scary. Then they wait. The market starts to recover, but they don’t quite trust it yet. It dips again, and that feels like confirmation they were right to stay out. Then it recovers again — and now it’s been a year and a half, and getting back in somehow feels riskier than staying on the sidelines.

I would say this is the most common pattern I see, and it’s not a personal failing. It’s human wiring. And it’s not a lack of discipline; often, it is the trap of an analytical mind trying to solve an unsolvable problem.

Behavioral finance has a name for it: loss aversion. The idea that the psychological pain of losing money is roughly twice as powerful as the pleasure of gaining it. So, when your portfolio drops 20%, your brain is registering something closer to a 40% loss. That imbalance is exactly why sitting in cash feels like safety, even when the math says otherwise.

The Part Nobody Talks About: The Compounding Cost of Missing the Recovery

Here’s where the conversation starts to get uncomfortable for a lot of clients.

When someone steps out of the market during a downturn, they often miss the beginning of the recovery. And that beginning is exactly when it matters most. Market rebounds don’t always happen gradually. They can occur in shorter periods of time. Take for example the COVID-19 Pandemic. According to FactSet, within five months from the S&P 500 closing at a previous high on February 19, 2020, the S&P 500 recovered its COVID crash losses on August 18, 2020.

I’ve shared this with clients before, and I think the reason it resonates is that it makes visible something that otherwise stays completely hidden: the cost of waiting. You can see a market decline on a chart. You can feel it in your stomach. But the recovery days you missed while sitting in cash? Those are invisible until it’s too late.

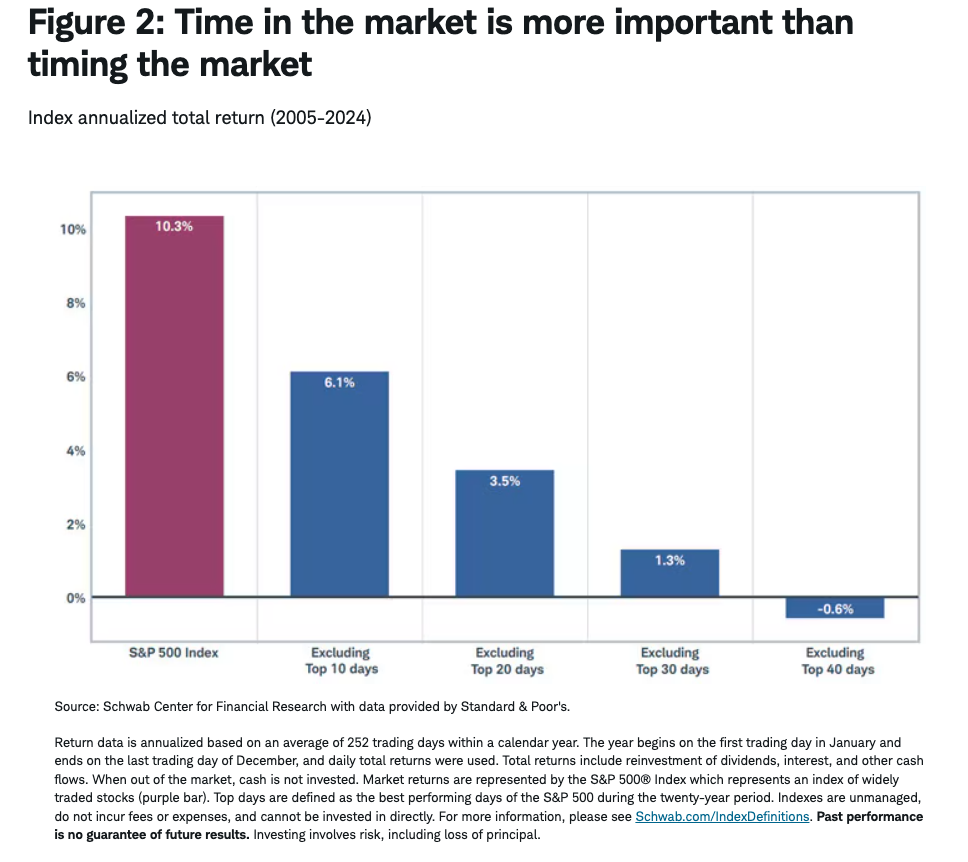

Below is another chart illustrating that missing just the 10 best trading days in the market over a 20-year period can cut your returns nearly in half.1

And here’s the part I feel is really important to understand: those best days in the market almost always show up right next to the worst ones. They’re clustered around exactly the moments when everything feels most uncertain. This means the people most likely to miss them are the ones sitting in cash, waiting for clarity that never quite arrives.

And here’s the part I feel is really important to understand: those best days in the market almost always show up right next to the worst ones. They’re clustered around exactly the moments when everything feels most uncertain. This means the people most likely to miss them are the ones sitting in cash, waiting for clarity that never quite arrives.

The Real Risk Was Never Volatility

This illustrates how clients didn’t lose money by staying invested in 2022. They lost money by selling, and then staying out while the market recovered. The portfolio he walked away from has since recovered and moved higher. The cash he was holding quietly lost purchasing power to inflation, year after year. And to get back in, he’d be buying at prices meaningfully higher than where he stepped out.

This is what I think about on behalf of clients more than anything else. Volatility is visible — it’s right there on the screen, it’s in the headlines, you can feel it in your stomach. But the cost of missing the recovery? That’s invisible. And by the time you see it, it’s already happened.

The question I ask clients in this situation isn’t “are you comfortable with what the market is doing right now?” It’s a different question: What is your cash actually costing you? Because doing nothing is still a decision. And it has a price.

“What is your cash actually costing you?”

Because doing nothing is still a decision. And it has a price.

What I Tell Clients in This Situation

I’m not going to tell you staying invested is always easy. It isn’t. There are moments, and we’ve lived through several of them in recent years, where every instinct you have wants to pull the lever and get out. That feeling is real. It’s valid. And it doesn’t make you a bad investor.

But what I have learned over time is that what separates investors who build generational wealth from those who don’t usually isn’t some ability to time the market. It’s the ability to stay in the plan when the plan feels uncomfortable.

And I would say that’s a big part of what a good wealth manager actually does — not just building a diversified portfolio that’s aligned with your goals, but helping the client rely on a disciplined investment process as well when uncertainty makes you want to do something. Anything.

Because the market doesn’t care how you feel right now. But your long-term financial plan does.

A Note If This Sounds Familiar

I’ve had these conversations many times, especially in the last year, and I never come to it with judgment.

What I can tell you is that there’s a way to re-enter thoughtfully — in stages, with a plan that considers your specific tax situation and timeline. The goal isn’t to make up for lost time overnight. It’s to stop compounding the cost of staying out.

If you’d like to talk through where you are, reach out. These are exactly the conversations I’m here for.

Brian Gigl, CFP®, CTFA

Director of Wealth Management

Riverwater Partners

Citations

The information provided herein reflects the opinions of Riverwater Partners, LLC as of the date of publication and is subject to change without notice. It is provided for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Investing involves risk, including the potential loss of principal. Indices cannot be invested in directly and are unmanaged. Riverwater Partners does not guarantee the accuracy or completeness of this information and is not responsible for any errors or omissions. Clients or prospective clients should consult their financial advisor before making any investment decisions. Riverwater Partners is a Registered Investment Advisor with the U.S. Securities and Exchange Commission (SEC).