Sustainability Disclosure in Small Caps: Another Dimension Where the Work Matters

In late 2024, we published our first comprehensive analysis of sustainability reporting across the Russell 2000, finding that roughly half of small-cap companies disclosed Environmental, Social and Governance data—a striking gap compared to the near-universal reporting among S&P 500 constituents. We’ve now updated that research, and the trends we identified have continued: disclosure rates have climbed modestly to 54%, but the structural gap between small and large caps persists. For managers who integrate sustainability considerations into their quality assessment—as we do at Riverwater—this gap has practical implications for risk management and due diligence.

The Disclosure Gap: 54% vs. Nearly 100%

The disparity in sustainability reporting between large and small caps is striking. Nearly all S&P 500 constituents publish formal sustainability reports—the figure approaches 100%.2 In contrast, only approximately 54% of Russell 2000 companies publish such reports, up modestly from around 50% in June 2024.3

The disparity in sustainability reporting between large and small caps is striking. Nearly all S&P 500 constituents publish formal sustainability reports—the figure approaches 100%.2 In contrast, only approximately 54% of Russell 2000 companies publish such reports, up modestly from around 50% in June 2024.3

This gap matters, though not in the same way the analyst coverage gap matters. Sparse sustainability disclosure does not directly create mispriced securities waiting to re-rate. But it does mean that nearly half the small-cap universe offers reduced visibility into governance quality, environmental liabilities, workforce practices, and other factors that can materially affect long-term business value.

For passive investors, this opacity is simply absorbed. An index fund owns the entire Russell 2000—companies with robust sustainability programs and companies with hidden risks alike. For active managers willing to dig deeper, the disclosure gap creates an opportunity to differentiate: avoiding companies with concealed liabilities while identifying well-governed businesses that happen to lack the resources for formal reporting.

Why This Matters: Risk Avoidance and Quality Signals

The value of sustainability analysis in small caps is less about finding hidden gems and more about avoiding hidden landmines.

Environmental liabilities, governance failures, labor disputes, supply chain vulnerabilities—these risks exist whether or not a company discloses them. When they surface, the market reaction can be severe. A company that has not reported on its environmental practices may be managing them well, or may be sitting on remediation costs that will eventually hit the balance sheet. Without disclosure, investors cannot distinguish between the two.

Active managers can bridge this gap through primary research: site visits, management interviews, employee reviews, supply chain analysis, and regulatory filings. This work does not guarantee alpha in the way that discovering an undervalued stock does. But it can prevent the kind of permanent capital impairment that comes from owning a company whose risks were invisible until they were not.

There is also a quality signal embedded in disclosure itself. Companies that invest in sustainability reporting tend to be companies that think about long-term value creation, stakeholder relationships, and business resilience. The act of measuring and reporting requires management attention and organizational capability. It is not a guarantee of quality, but it correlates with the kind of thoughtful management we look for.

The relationship between disclosure and quality shows up in financial performance as well. Among Russell 2000 constituents, 61% of profitable companies publish sustainability reports, compared to just 44% of unprofitable ones.8 This correlation runs in both directions: companies with resources to invest in reporting tend to be more profitable, and the organizational discipline required to measure and disclose sustainability factors often accompanies the kind of management focus that drives profitability.

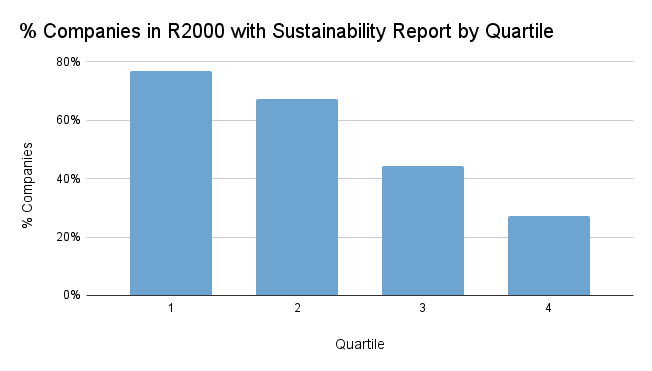

Size Matters: The Resource Constraint Reality

Why does the disclosure gap persist? The answer lies in resource constraints that are structural, not temporary.

Within the Russell 2000, sustainability reporting correlates strongly with company size. In the largest market cap quartile, over 77% of companies publish sustainability reports. In the smallest quartile, that figure drops to just 27%.4 This gradient reflects a fundamental reality: producing high-quality sustainability disclosures requires dedicated staff, robust data collection systems, and expertise in reporting frameworks. Smaller companies often lack these resources.

This is not a market inefficiency that will be arbitraged away. It is a permanent feature of the landscape. Even as overall disclosure rates improve, smaller companies will continue to lag larger ones because the resource constraints are real. For active managers, this means the due diligence burden in small caps will remain higher than in large caps indefinitely.

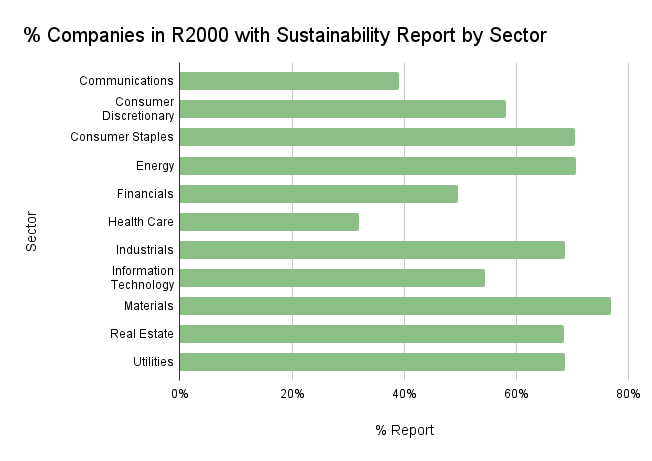

Sector Variation: Disclosure Does Not Equal Risk

Sustainability disclosure varies significantly by sector, but not in ways that align with actual sustainability risk. Industries with more visible environmental footprints tend to have higher reporting rates: Materials (77%), Energy (71%), and Consumer Staples (70%) lead in disclosure.5 Service-based sectors lag, with Communications at 39% and Healthcare at just 32%.

This pattern reflects stakeholder pressure more than actual risk. Energy companies face obvious scrutiny on environmental practices, so they report. But Healthcare companies—with their complex supply chains, clinical trial ethics, pricing practices, and workforce considerations—face equally material sustainability issues. The low disclosure rate in Healthcare does not mean fewer considerations exist; it means those considerations require more work to assess.

Framework Preferences: SASB Leads

Small-cap companies use a variety of reporting frameworks to disclose their sustainability efforts. Our data reveals that among Russell 2000 companies that do report, the Sustainability Accounting Standards Board (SASB) framework dominates, used by 35% of reporting companies. The Global Reporting Initiative (GRI) trails at approximately 20%.6

SASB’s prevalence among small caps makes sense. Its industry-specific approach focuses on financially material sustainability factors—the issues most likely to affect enterprise value. For resource-constrained companies choosing where to focus limited disclosure efforts, SASB offers a pragmatic path: identify what matters most for your industry, report on that, and defer the comprehensive stakeholder mapping that GRI requires.

This preference aligns with how we approach sustainability at Riverwater. We are not looking for companies that check every responsible investing box. We are looking for companies where management understands which sustainability factors are material to their business and manages them thoughtfully. SASB’s materiality focus reflects the same priority.

Progress Despite Headwinds

Despite a political environment that has grown more skeptical of sustainability initiatives, disclosure rates among Russell 2000 companies continue to climb—up from approximately 50% to 54% over the past year.7

This suggests that sustainability reporting has become embedded in corporate practice. Companies that have built disclosure infrastructure are unlikely to abandon it. And as more small caps grow into the size ranges where reporting becomes standard, the overall rate should continue rising.

For active managers, improving disclosure is a mixed development. More data is generally better. But the transition will be uneven, and the gap between small and large caps will persist for years. Managers who have developed capabilities to assess sustainability factors—through primary research rather than reliance on disclosed data—will retain an advantage in the substantial portion of the universe where disclosure remains limited.

Our Approach: Due Diligence, Engagement, Collaboration

The disclosure gap reinforces why we built our responsible investing framework the way we did. At Riverwater, sustainability evaluation is not a screen applied after security selection—it is embedded in our process from the start through three pillars: Due Diligence, Engagement, and Collaboration.

Due Diligence comes first. We use a proprietary 25-point scoring system that evaluates 18 specific factors across environmental, social, and governance categories—everything from water stewardship and GHG emissions to board independence and executive pay alignment. Crucially, we weight these scores by industry (environmental factors matter more for manufacturers; social factors for service companies) and adjust for company size. Smaller companies receive credit for demonstrating progress even when they lack the resources for comprehensive reporting. We are not penalizing companies for being small; we are evaluating whether they are managing material risks appropriately given their scale.

Engagement follows naturally from our small-cap focus. Because we specialize in smaller companies, we often encounter management teams early in their sustainability journeys. We approach this as active owners, not activists—providing educational resources, encouraging adoption of frameworks like SASB and TCFD, and helping companies identify which responsible investment factors are most material to their specific business. When we vote proxies, we vote our convictions, including against management on governance issues when warranted.

Collaboration extends our reach. Through partnerships with organizations like CDP, Ceres, the UN Principles for Responsible Investment, and The Water Council, we both inform our own practice and contribute to broader efforts to improve corporate sustainability. Our Milwaukee roots have made water stewardship a particular focus—we actively refer portfolio companies to resources that can help them better manage water risk.

This framework exists precisely because we cannot rely on disclosed data alone. In a universe where 46% of companies publish no formal sustainability information, waiting for disclosure means missing both risks and opportunities. Our process is designed to generate the insight that disclosure does not provide.

Sustainability analysis in small caps is not about finding alpha in the way that discovering an undervalued stock is. It is about understanding the full picture of a business—its risks, its governance, its resilience. In a market segment defined by limited information, that understanding is another dimension where fundamental research earns its keep.

Citations

This material is for informational purposes only and does not constitute investment advice or an offer to sell or a solicitation of an offer to buy any security. The information presented reflects Riverwater Partners’ analysis of publicly available data as of January 2026; methodology available upon request. Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. For more information about Riverwater Partners, including our services, fees, and investment strategies, please see our Form ADV Part 2A or contact us at 414.858.8000.